Credit is a measure of how trustworthy you are with borrowed money. If you’re building credit from scratch, think of it as setting up your personal finance report card.

Before kicking things off, getting familiar with why credit matters is key. Everyone talks about credit scores, but why are they so important? Well, your credit score can make or break big life decisions, like snagging a good rate on a mortgage or even landing a job. Banks and lenders use it to determine your ability to repay the loan.

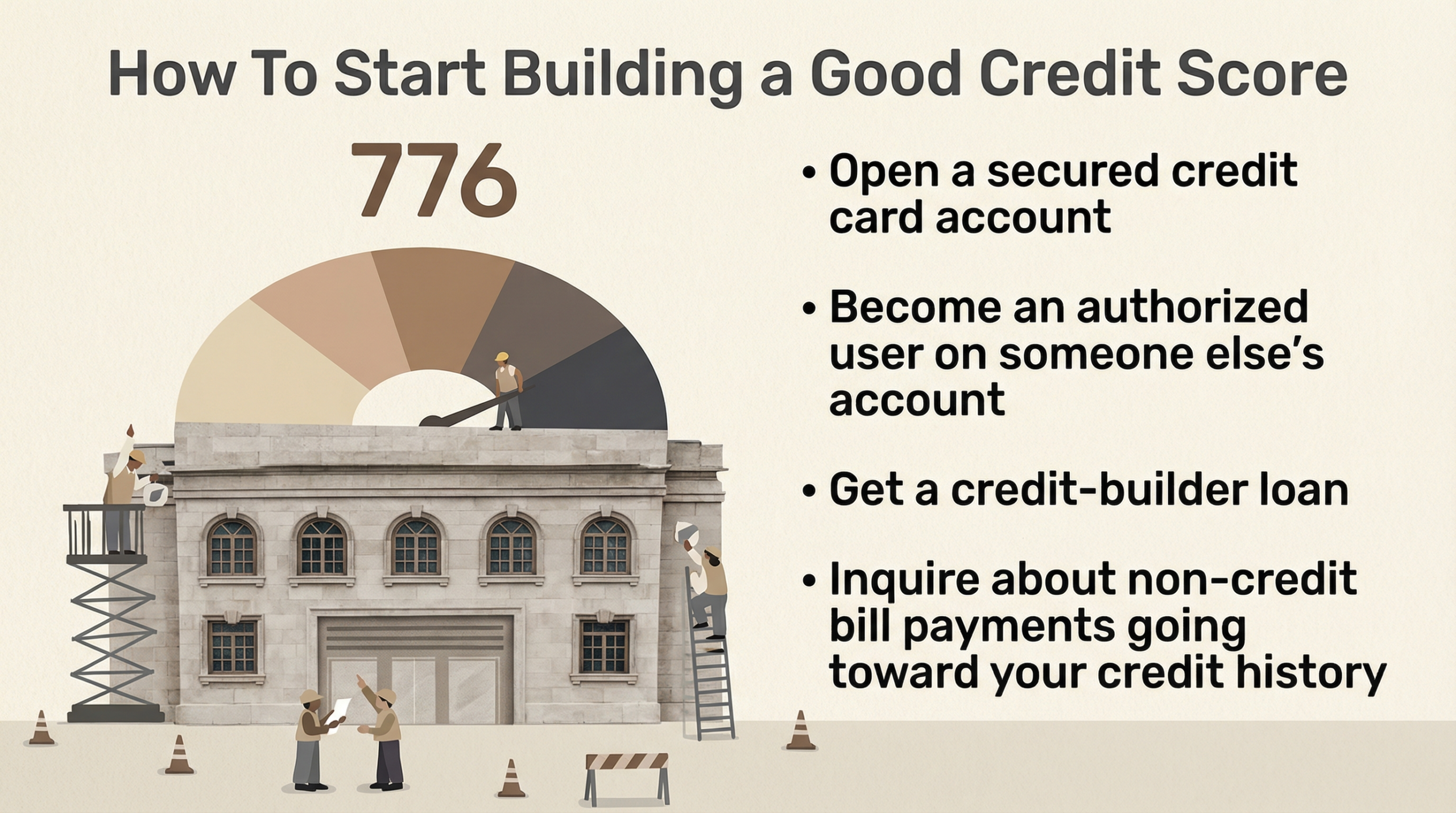

So, what’s the game plan for those just starting out? You might hear a lot about credit cards, loans, and credit scores flying around the place. But don’t sweat it—you won’t need them all right off the bat. Start simple with the tools at your disposal, like a secured credit card or a small credit-builder loan, to get the ball rolling.

Misconceptions? Yeah, there are plenty of those around. Building credit doesn’t happen overnight, no matter what your uncle said about dodgy shortcuts. Also, not using credit at all doesn’t save you from trouble. It’s about responsibly handling small amounts first, and being consistent.

Hammer this in: patience and strategy are your friends. Your score gets better with time and good habits, not by trying to game the system. Trust this process, and your credit will reflect the solid and genuine financial reputation you’re cultivating.

Quickstart Strategies: The Fastest Ways to Build Credit From Scratch

Getting credit up and running quickly isn’t just about patience, it’s about using the right tools. Secured credit cards can be your fast-track ticket. With these, you put down a deposit that becomes your credit limit. It’s low risk for lenders since they already have your cash, and it gives you a shot at showing you can handle credit responsibly.

Another nifty trick up your sleeve? Experian Boost. It’s for real—they use your phone and utility bills to boost your credit score. It’s like getting credit for stuff you’re already paying. No extra spending required.

Becoming an authorized user on someone else’s credit card account can help too. So, if there’s a trustworthy mom, dad, or buddy with a stellar credit record, see if they’re cool with it. You’ll piggyback on their good credit habits which is great if you’re just getting started yourself.

So, when you’re asking, “What is the fastest way to build credit from scratch?” Focus on these tools. They’re practical, manageable, and designed to set you off on the right path without the headache. Just remember, use these strategies in moderation—no need to juggle all at once.

Understanding Credit Scoring: How to Prepare for Major Purchases

Alright, let’s talk credit scores and why they matter. Picture them as your adulting GPA, a three-digit snapshot of how well you handle debt. It’s like a financial selfie to lenders. So, if buying a house is on your bucket list, here’s what you should know.

For most standard loans, you’d be eyeing a credit score of 620 and up. But the higher, the better—because better scores unlock better interest rates. That entails lower monthly payments and less cash shelled out over the life of a loan. So, yeah, there’s good reason to aim high with your score.

Knowing the difference between installment credit and revolving credit is useful too. Installment is fixed payments—think car loans. Revolving means regular, varying payments—credit cards most days. A mix of both shows lenders you can handle different kinds of debt.

By now, getting a sense of why building smart from scratch pays off is clear. Your payment history makes up a solid 35% of your credit score. New to this world? Start small, make each payment on time, and you’re golden.

Use these pointers. They might sound basic, but they’re the foundation for any big-ticket dreams like home ownership. Knowing where you stand with your credit is powerful stuff, and it could save your wallet a ton in the long run.

Developing a Sustainable Credit Strategy

So, you want your credit to not just pop, but stay solid for the long haul. Enter the ‘2 2 2 credit rule.’ It’s like simplifying success: have two credit cards, keep balances under 20% of the limits, and make sure they’re open for at least two years. Simple but effective, right? It’s a way to show stability and smart management to the money folks.

Building credit if you have none sounds tricky, but it’s not a lost cause. Start with small amounts, like a manageable loan, and hit that monthly due like clockwork. You’re crafting a financial narrative, so keep it consistent and positive.

Good habits are your backbone here. Pay those bills on time, keep debts reasonable, and avoid going on wild spending sprees. It’s about shaping a lifestyle that naturally boosts credit without too much stress.

Pay attention to your score updates. Regularly peek at your credit report for any slip-ups, and don’t shy away from asking for a pro’s help if you hit a snag. They can offer tips focused on your particular situation and goals.

Remember, the pathway to strong credit isn’t about perfection overnight; it’s about steady, informed decisions and sticking to practices that build trust with lenders over time.