Student loans can be a bit of a mystery, so let’s break down the essentials. There are two main types: federal loans, which are offered by the government, and private loans, which come from banks or other institutions. Federal loans usually offer more flexible repayment options and lower interest rates, making them a popular choice for many students.

Speaking of interest rates, they play a massive role in how much you’ll end up paying over time. Federal loans typically have fixed rates, meaning they stay the same throughout the life of the loan. Private loans might have fixed or variable rates, which can change over time and affect your payment amounts.

Now, you might hear about loan consolidation and refinancing a lot. Consolidation combines multiple federal loans into one, possibly lowering your monthly payment, but it might not save you money over time. Refinancing, on the other hand, can lower interest rates but is usually only available for those with strong credit and steady income.

Federal student loan service providers are the entities that handle the billing and other services. Knowing who your servicer is, and how they operate, is key in managing your loans. They’re your go-to for questions about how to pay or if you’ve got trouble making ends meet.

Lastly, let’s consider the bigger picture: how student loans affect your financial health. They’re a significant part of your credit history and can impact your credit score. It’s crucial to understand your repayment obligations to keep your credit in a healthy place while paying off your loans.

Common Mistakes to Avoid When Managing Student Loans

Avoiding certain missteps can save a lot of hassles in loan management. Missing payments is a no-go. Not only do you rack up extra costs, but your credit score takes a hit, which affects future borrowing or lease applications. Prioritizing timely payments helps maintain a healthy financial standing.

Income-driven plans are amazing tools but can be misunderstood. They promise low monthly payments based on your earnings, but extending the repayment period means you might pay more in the long run. It’s crucial to really understand how these plans work and their long term effects.

Deferment can seem like a temporary breather, but defer too much, and interest might capitalize, increasing your balance. It’s critical to be strategic about when to use deferment to avoid adding unnecessary costs.

Interest capitalization is another hidden danger. Any unpaid interest in deferment may be added to your principal, compounding your debt. Keep an eye out for when this happens and try to manage payments to avoid the extra burden.

Ignoring rising interest rates can lead to surprises down the road, especially with private loans. Keep an eye on economic news related to interest trends so you’re prepared for any changes that might affect what you owe. Always stay engaged with your loans to anticipate shifts in your repayment expectations.

Mapping Your Repayment Timeline and Plans

Repayment plans can be tricky, but knowing your options is half the battle. Standard plans are pretty straightforward; you make fixed payments over ten years. Graduated ones start low, then increase, which can be handy if you’re expecting future income growth. Extended plans offer more leeway with up to 25 years to repay, reducing monthly bills, but they might cost more in the long run.

Income-driven plans deserve attention if you’re weighing flexibility and affordability. They adjust payments based on your earnings, which helps if you’re starting on a lower salary. But remember, extending repayment terms can mean paying more overall, so weigh these decisions carefully.

Loan forgiveness programs are golden tickets for some, especially those in public service or teaching. Check eligibility criteria because not everyone qualifies, and certain jobs or payment plans might not count, so planning ahead is key.

Deferment and forbearance come in handy during tough times, sudden job loss or medical issues, for instance. However, use these options carefully to avoid additional costs like interest capitalization, which adds to what you owe.

Keeping on schedule with payments is foundational. Missing one can hurt your credit score, and falling into default brings long term financial headaches. Building a repayment timeline that maps out different phases of your life can help keep everything on track.

Advanced Strategies to Pay Off Your Loans Faster

Tackling student loans quickly can free up funds for other goals, so let’s explore some smart strategies. Begin with a solid budget that prioritizes your loan payments. This might require cutting back on nonessentials, but the payoff is worth it.

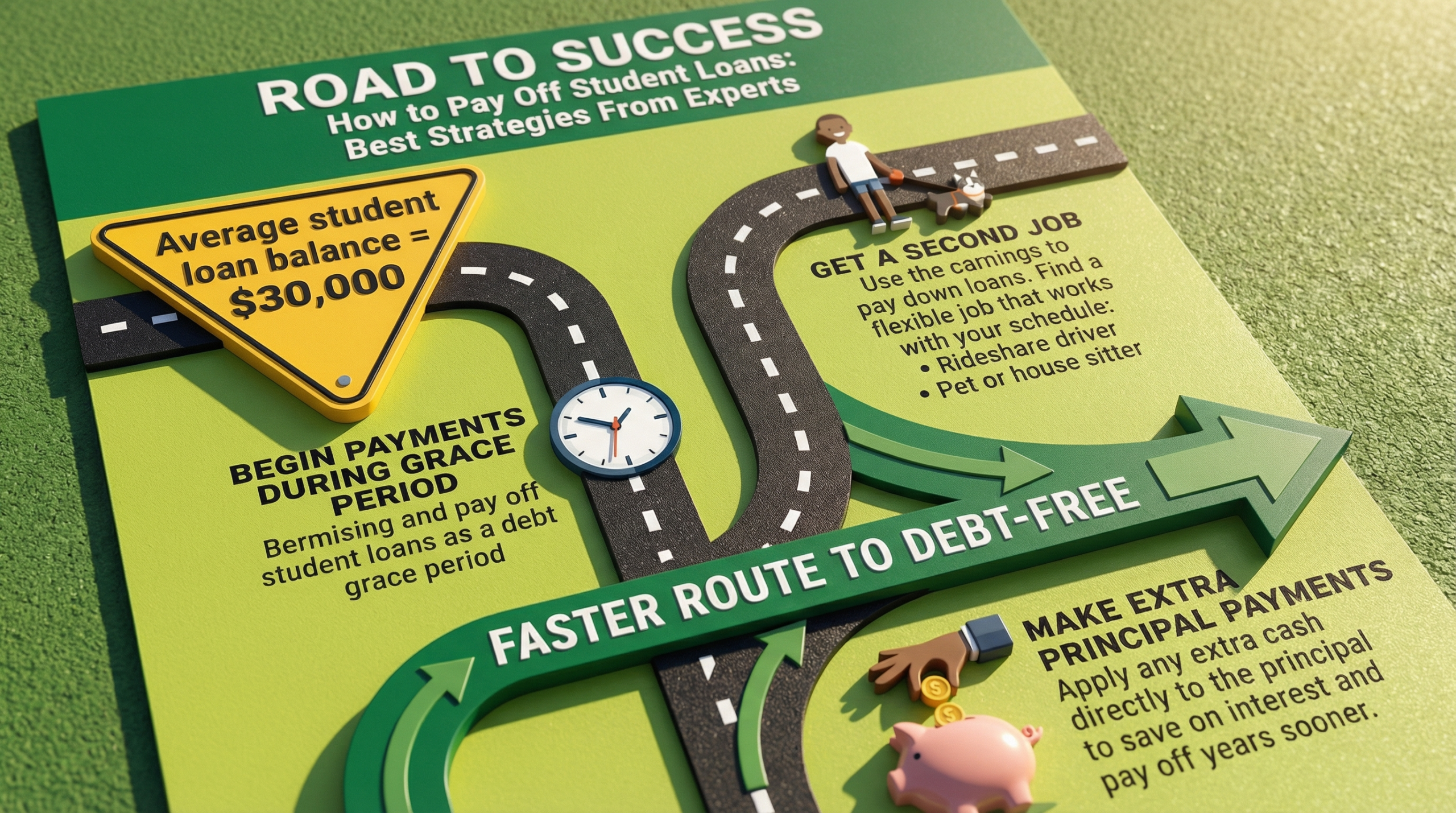

Boosting your income through side hustles or parttime jobs can be a game changer. The extra cash can directly fund your loans, helping shorten the loan lifespan, and reduce interest costs.

When it comes to prepaying loans, consider adding extra to your monthly payments or making a lump sum payment when you can. Even small additional amounts can significantly reduce your debt burden over time.

Some employers offer student loan repayment assistance as part of their benefits package, so it’s worth investigating if your employer can help chip in.

Refinancing can lower your interest rates, especially if your financial situation has improved since you took out your loans. Just ensure the new terms align with your repayment goals, as refinancing federal loans turns them into private ones, which may remove certain protections.

Using these strategies can diminish those numbers on your debt balance faster than you think. A combo of budgeting, extra income, and savvy repayment choices works wonders.

Building Healthy Financial Habits for a Debt Free Future

Crafting a robust financial plan is like setting a roadmap to ensure all your money goals are within reach. Stick to your plan, adjusting as life changes, and you’re more likely to stay on track with repayments.

Balancing loan payments with other goals like saving for retirement or emergencies is crucial. A well rounded financial strategy prevents loans from overshadowing other important areas of your financial life.

Staying disciplined about avoiding new, unnecessary debt keeps your financial health in check, saving you from future headaches. Being cautious about using credit makes repayments more manageable.

An emergency fund acts as a safety net, ensuring that unexpected expenses don’t derail your student loan journey. Aim to save a modest amount regularly, gradually building a cushion over time.

As you manage your loans, building credit responsibly can open doors to better financial opportunities later. Pay on time and avoid maxing out credit cards to keep a favorable credit profile.