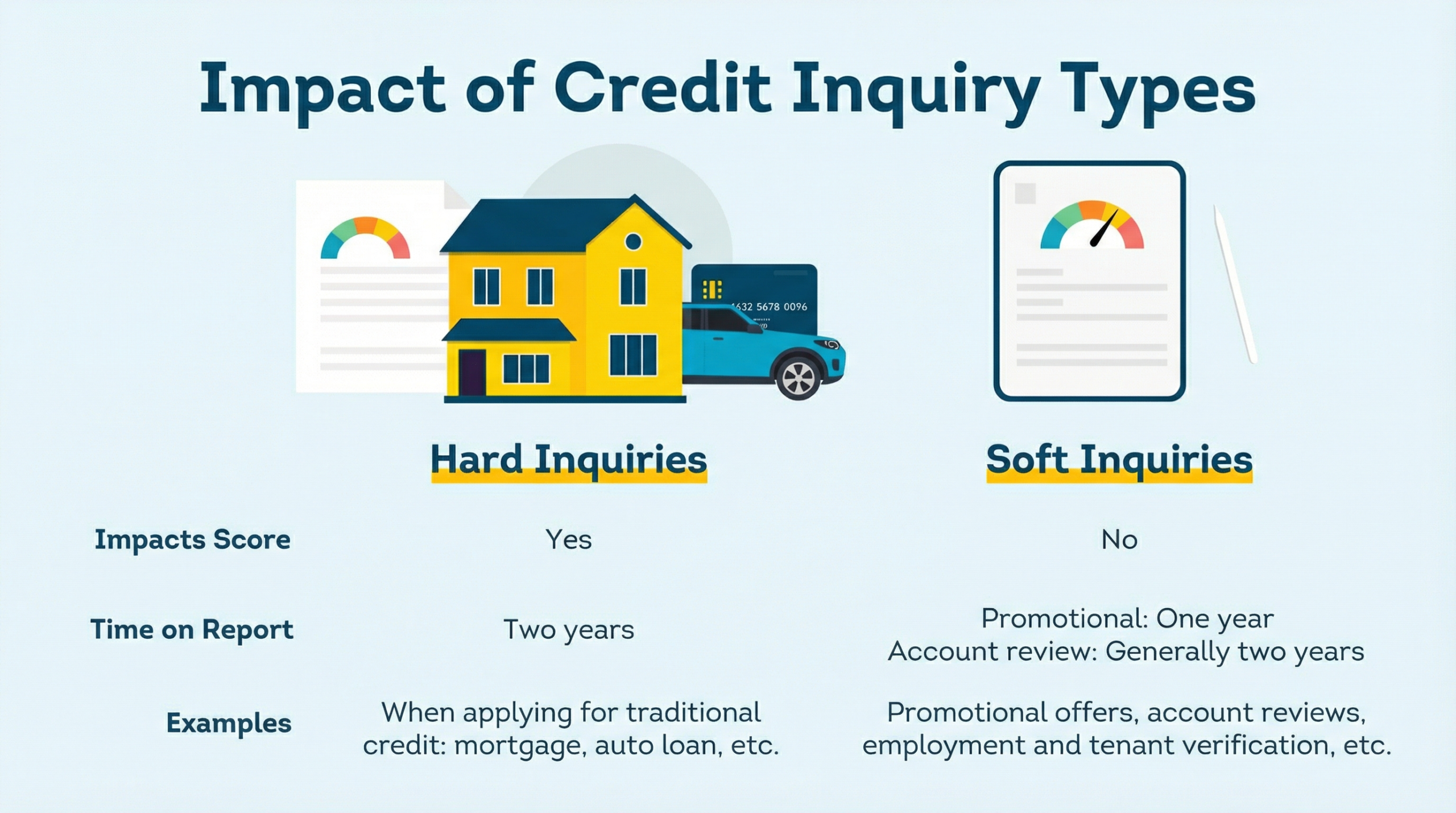

Credit inquiries are a pretty big deal in the world of finance. They’re those checks into your credit history and come in two flavors: hard and soft. Let’s break these down. A hard inquiry, or hard pull, happens when a lender checks your credit to make a lending decision. Think applying for a mortgage, credit card, or car loan. Meanwhile, a soft inquiry, or soft pull, is more like a background check. They don’t affect your credit score and usually happen when you’re checking your own score or when lenders want to pre-approve you for some sweet deals.

So, what’s the big difference? Hard inquiries can slightly ding your credit score because they signal you’re looking to take on new debt, which can be seen as a bigger risk by lenders. Soft inquiries are harmless. They’re usually hidden from potential lenders (except, of course, yourself) and don’t impact your financial health or lending capabilities.

Everyday situations embody these concepts. If you’re tracking your own credit score using a free service or if a company checks your score for a pre-approved offer without your formal application, that’s a soft inquiry. On the other hand, formally applying for an auto loan and triggering a credit check? That’s hard, my friend.

Understanding these inquiries helps. It means knowing when you’re opening the door to a possible score change and when it’s just a casual peek. Hard inquiries stay on your credit report for up to two years, so it’s good to be strategic about when and why you allow them. Soft inquiries? No sweat—track those all you want.

How Credit Inquiries Influence Your Credit Score

Ever wondered if those credit checks are pulling the strings behind your credit score? That’s the magic of inquiries. Hard inquiries can impact your score because they often signal to lenders that you’re on the hunt for credit. Generally, each hard pull can shave off a few points—and if you’re racking up multiple within a short time, it might show you’re a bustling bee in the credit garden, which could be a red flag.

Soft inquiries, on the contrary, are harmless when it comes to your credit score. They happen often and without consequence—like when you peek at your own credit or those pre-approval offers land in your mailbox. So, while it’s good to be aware of the soft ones, they’re not the villains in this story.

Credit bureaus like Experian, Equifax, and TransUnion keep tabs on these inquiries. When they update your credit report, every hard inquiry shows up, noted boldly for lenders to see. It typically impacts your score for about a year, though they’ll stay visible on your report for up to two years. With soft inquiries, you’ll see them in a personal credit check, but they don’t factor into your score calculation.

So, what’s the strategy here? Be mindful of applying for credit too often. Concentrating your potential inquiries over a short burst—like searching for the best mortgage or auto loan rates—can be bundled together in what’s often called a “rate-shopping” period. This doesn’t allow your score to take unnecessary hits each time, keeping your financial health in check.

Unveiling Credit Myths: The 2-2-2 Credit Rule Explained

Ever hear about the 2-2-2 credit rule? It’s like one of those secret handshakes in the world of credit management, yet it’s not official policy but rather a guideline many find useful. So, what’s the deal with this rule?

The 2-2-2 credit rule refers to maintaining at least two credit accounts, each with a two-year history and a minimum two-year gap since your last negative mark. The idea is to show lenders you’re a reliable borrower.

Breaking it down: the first ‘2’ is about keeping two active credit lines. The second ‘2’ suggests those accounts should have a history spanning two years, boosting your credit stability and reliability. The last ‘2’ means steering clear of troubling financial hiccups, such as late payments, for two years. This paints a picture of responsibility and consistency for lenders.

But is this rule a golden ticket? While it can be helpful, it’s not a one-size-fits-all solution. Credit scores also consider factors like credit utilization, recent inquiries, and the variety of credit types you manage.

Following this rule doesn’t assure instant approval—lenders have their own criteria. However, using it as a guide helps maintain a balanced credit profile, which is always a step in the right direction! Consider this rule like guardrails, keeping your credit journey steady and on track.

Assessing the Risks: Are Hard Inquiries Damaging?

Wondering about the impact of hard inquiries? They’re those credit checks that happen when lenders assess you for a new credit line. They might seem small, but they can actually influence your financial health.

Hard inquiries get a bad rap because they can affect your credit score, albeit slightly, usually taking off a few points. This happens because lenders start to wonder why you’re seeking new credit and if you’re biting off more than you can chew. They view it as a risk, especially if there are multiple inquiries in quick succession.

But are they really damaging? Not necessarily. In the grand scheme, they’re just one piece of the credit score puzzle. Things like your payment history, credit utilization, and account age carry more weight. A well-rounded credit profile doesn’t get shaken up by a few inquiries here and there.

To keep the impact low, it’s all about strategy. Only apply for credit when you need it and do your research beforehand to know what you’re eligible for, helping you avoid unnecessary hard pulls. Focus on boosting your credit profile with on-time payments and responsible borrowing rather than stressing over every inquiry.

Remember, these inquiries stay on your report for about two years but only affect your score for around one year. So, managing them wisely helps keep your financial outlook bright and healthy.

Navigating Multiple Inquiries: Is Having 7 Hard Inquiries Bad?

Seeing a bunch of hard inquiries on your credit report can be alarming, especially if you’ve got around seven of them lined up. But let’s unpack how bad that really is.

First off, context matters. Multiple inquiries in a short span can signal to lenders you’re actively seeking credit, which might indicate financial stability issues. However, there’s also grace in numbers. Credit scoring models often account for “rate shopping,” especially with mortgages and auto loans, by lumping similar inquiries made within a specific time frame together. This means, when you’re finding the best deal, those inquiries may only count as one.

Now, what about worrying if you’ve exceeded a certain number of inquiries? Generally, five or more in a year might bump you into a riskier category from a lender’s perspective, particularly if they see no new accounts resulting from those inquiries. But seven inquiries don’t spell disaster. It’s more about patterns over time rather than a strict count.

Managing these inquiries means planning your credit applications. Space them out where possible and ensure your financial affairs are in order before applying. Stay strategic–only pursue credit lines that make sense for your goals and don’t overextend your borrowing capacity.

If you’ve already amassed several inquiries, concentrate on other credit score factors. Strengthening your payment history, reducing credit card balances, and maintaining a mix of credit types can bolster your profile, balancing out any effects from these inquiries. With a solid approach, even seven inquiries on record won’t anchor you down.